onity group

INITIAL PUCHASE DATE: Sept 28, 2025 INITIAL PURCHASE PRICE: $40.98

UPDATE: May 27, 2026 CURRENT PRICE: $36.00

The Business

Onity Group (Ticker: ONIT) is a financial services company focused on originating and servicing forward and reverse mortgage loans, primarily in the United States. In 2025, the company generated $1.2 billion in revenue, $189m in net income, and $69.5 million in adjusted net income. Onity operates in a competitive and consolidating mortgage servicing industry.

The Simple Value Story

Onity’s history has been turbulent. Following the Great Recession, its founder and then-CEO pursued an overly aggressive foreclosure strategy that backfired, saddling the company with lawsuits, regulatory penalties, and heavy debt. In 2018, Onity acquired PFF and appointed PFF’s CEO, Glen Messina, to lead the combined firm. Since then, Messina has streamlined operations, refinanced debt, and returned the company to profitability and stability.

Despite this turnaround, the market continues to undervalue Onity.

First, Onity’s current tangible book value is $629 million[1], compared with a market capitalization of $301 million. If the market simply re-rated Onity to book value, the stock would increase from its current $36 per share to $75, a 108% increase.

Second, over the past four quarters, Onity has generated adjusted net income approximately $55.1m (excluding the $120m in deferred tax adjustments). There was nothing exceptional about net income in 2026. In fact, both Q4, 2025 and Q1, 2026 were below the average of roughly $20m earning in each of the first three quarters 0f 2025 due to runoffs resulting from FHA rule changes and the government shutdown (these runoffs are expected stabilize in Q2). Even at the temporarily reduced net income of $55m, a PE of 10 would result in a market cap of $550m, and 82% increase in the market price. Under the assumption that steady state net income is $70m per year, a PE multiple of 10 would result in a market cap of $700m, and a stock price of $82 per share, and a 127% increase in the stock price.

Third, Onity looks quite inexpensive relative to the price paid for Mr. Cooper, another mortgage servicing company. Mr. Cooper was bought out by Rocket Companies in October 2025. At the time of the initial announcement Rocket offered stock worth $9.4B, or 14 times Mr. Copper’s prior year net income and over 2 times its tangible book value. NOTE: By the time of closing Rocket’s stock had appreciated, so that its effect price to purchase Mr. Cooper was $14.2B.

Discussion

Onity makes money in several ways. The most important is as a mortgage servicer. As a mortgage servicer, it collects monthly payments, manages escrow accounts, handles delinquencies, and processes foreclosures. For these functions, Onity earns recurring fees tied to the outstanding principal balance of the mortgages it services. As of the end of Q1, 2026, it services $338 billion in mortgages, an increase of 11% over 12 months (roughly 26% of a $13.2trillion market). Importantly, servicers like Onity do not assume credit risk on these mortgages; the owner of the loan bears that risk.

Mortgage servicing rights (MSRs) are valuable assets. Onity acquires them through its own originations, through purchases from large mortgage holders, and via competitive bidding. At the end of Q1 2026, Onity owned servicing rights to $338 billion of underlying mortgages, carried at a fair value of $3.03 billion. This carrying value is marked-to-market each quarter, primarily reflecting interest rate movements. When rates fall, refinancing activity rises, shortening the life of the mortgage and reducing MSR value.

Onity also originates new mortgages — about $43 billion in 2025. These loans are typically sold quickly after origination, with Onity retaining the MSRs. At Q4, 2025, for example, the company held just $1.9 billion in loans for sale. Because the loans are sold rapidly, Onity faces minimal interest rate or default risk on its originated portfolio.

The company also maintains a meaningful presence in reverse mortgages, originating, servicing, and holding approximately $9.6 billion. Here too, Onity earns steady fees across the lifecycle of the loan. While repayment timing is uncertain — it depends on property sales or borrower death — the company is contractually entitled to all fees and is guaranteed reimbursement by the federal government if loan balances exceed property value.

The principal risk to Onity is interest rate volatility. Falling rates drive refinancing that erodes MSR value. To mitigate this, Onity both hedges with swaps and derivatives and benefits from a natural offset: when refinancing surges, its origination business expands, generating fresh fee income and replenishing MSRs. Hedging does not fully eliminate exposure, but it helps stabilize results.

Ultimately, Onity’s model is straightforward: originate mortgages, sell them while retaining MSRs, efficiently service both forward and reverse mortgages, and use scale to operate more profitably than peers.

Over the remaining sections I go through some of the details of Onity’s operations and financial statements.

Reverse Mortgages and Loans Held for Investment

Onity engages in reverse mortgages. Typically, reverse mortgages are taken out by senior citizens that own their houses outright, but don’t have cash flow. Onity provides the cash, and the house serves as the collateral. Every month that the reverse mortgage exists, more of the house principal is transferred to Onity. The mortgage owed to Onity is repaid when the house is sold, either at the choice of the owner, or upon their death. Onity is only owed the outstanding cash plus interest – there is no windfall gains possible. If the owner outlives the value of their house, the Home Equity Conversion Mortgage program, operated through the Federal Housing Administration, guarantees the payments. There is no risk of default risk or loss of funds to Onity.

Note that Onity is in the process of selling the majority of its reverse mortgage business. Onity announced in Q4 that it was selling the entirety of the reverse mortgage business to Finance of America Reverse for net proceeds and increase in assets of $100m (Onity would retain the servicing rights to the $9.6B in reverse mortgages). However, Ginnie May did not approve of the transaction. The amended deal is for Onity to sell 54% of the reverse mortgage business $105 in gross cash proceeds and $70m in net proceeds. Of course, this latest agreement is subject to government approval.

There are several benefits of this deal. First, Onity obtains cash and an increase in book value. Second, Onity will be able to decrease the debt on its balance sheet. Third, Onity will be able to simplify its operations.

There are two important outcomes from this transaction. First, the transaction will eliminate both the HECM assets and the offsetting HMBS liabilities of $9.6B: Onity’s balance sheet will shrink both assets and liabilities by $9.6B. This should screen much better. Second, Onity will receive approximately $100m of cash from the transaction. Onity has stated that it will use the cash for debt repayment and share repurchases.

Mezzanine Equity

At Q4, 2024, Onity issued $49.9m of Series B, preferred shares. These shares were used to raise approximately $50m in cash. These funds are recorded as mezzanine equity. Mezzanine equity has features of both debt and equity. These liabilities have the right to receive 7.875% interest payable in quarterly dividends for five years, after which the interest rate grows by 2.5% per year, to a maximum of 15%. On or after September 15, 2028, Onity has the right to redeem the entirety of this equity for $50m, plus any outstanding interest. I treat this as debt.

Debt Refinance in Q4, 2024

In Q4, 2024, Onity refinanced or repaid $685m of outstanding debt. The early repayment and refinancing of this debt resulted in a net one-time accounting loss of $49.9m. The upsides of this refinancing were lower debt and lower average interest rates.

However, one effect of the $49.9m write down is that Q4 earnings were -$28.1m. Without the $49.9m write down, Onity would have shown a profit of roughly $15m in Q4.

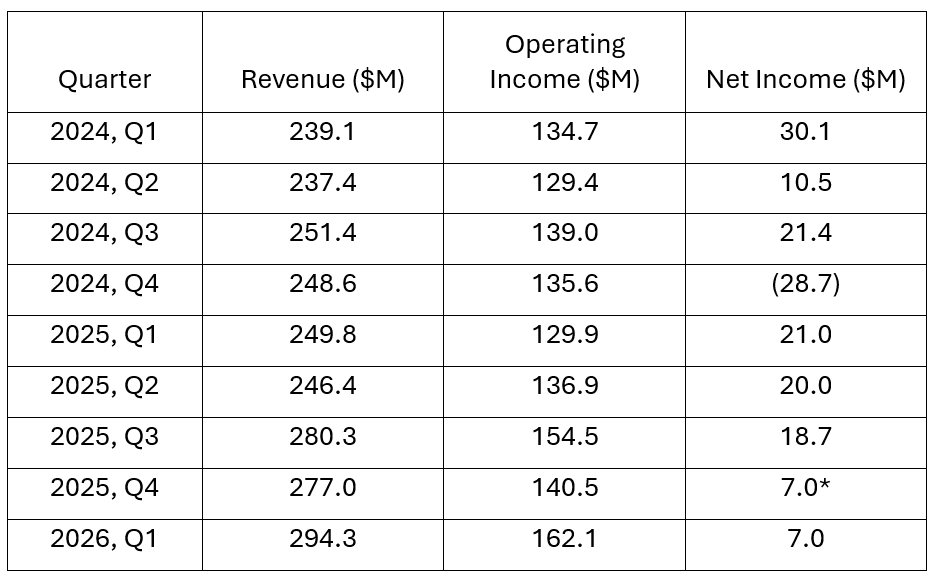

Steady State Earnings

Here are Onity’s net income and EBIT for the last nine quarters:

As explained previously, the $28.7m loss in Q4, 2024 was due to refinancing debt early. Other than this loss, it appears that Onity has stabilized its earnings.

* For this amount the $120m operating loss tax reversal was subtracted from the reported $127m in net income. The decrease relative to prior quarters is due to the government shutdown in Q4 and the FHQ rule change (as discussed previously).

Outstanding Stock Warrants

At Q4, 2024, Onity had 261,248 warrants outstanding to Oaktree with a strike price of $24.31, expiring on May 3, 2025. On Feb 3, 2025, Oaktree exercised the options. Rather than issue new shares, Onity elected to settle in cash for $3.5m.

On Dec 5, 2025, Oaktree exercised the 1,184,768-share warrant at $26.82. Onity elected to settle in shares via net share settlement, issuing 462,762 net shares (representing 5.4% of outstanding shares at the time).

At this point, Onity has no remaining warrants outstanding.

Stock Repurchases

On November 20, 2022, Onity repurchased 1,750,557 shares at an average price of $28.53, and a total price of $50m. This, and the recent settlement of the outstanding warrants, are the only shares Onity has repurchased in the last 5 years.

In the 2025 10-K, Onity announced that it would release $10m for share repurchases. It then used the entire $10m to repurchase shares during Q1, 2026.

Onity indicated that once the reverse mortgage were sold there would be $100m in additional cash, one purpose of which was repurchasing shares.

Shares Outstanding

At the end of Q1, 2026, Onity had 8.41m shares outstanding.

Management

In my opinion management has done a very good job over the last 8 years. The CEO, Glen Messina, joined Onity when Onity purchased PFF Corporation in 2018. Since that time Messina has been improving operations and cleaning up the balance sheet. At this point these efforts are largely complete.

The refinancing steps taken in Q4, 2024 have effectively eliminated the balance sheet risk to the company, and reduced interest rates.

All warrants are settled.

The balance sheet will be further simplified with the sale of its reverse mortgage business.

Current management has done an excellent job of running operations over the last 8 years.

I am pleased with the way management has treated shares. It completed a major stock repurchase when the stock price was at its lowest point. Rather than issue more shares when Oaktree exercised its options in Q1, 2025, management simply bought out the shares. In Q1, 2025, management used its limited $10m in excess cash to quickly repurchase shares. While this may be my bias, I believe that management will use a large fraction of any excess cash from its sale of the reverse mortgages to repurchase shares.

Valuation

Onity forecasts a pre-tax return on equity of 13-15% in 2026. At 14% that indicates $88m in pre-tax income. Onity also indicates a 28% tax rate, so net income forecast of $63m. At PE=10 this is $630m. With 8.41m shares outstanding the price would be $74.

Current tangible book value is $629m, or $73.70 per share (almost identical to the estimate based on PE=10).

An additional $63m in net income would increase Onity’s tangible book value by the end of 2026 to $691m, or $81.10 per share.

Conclusion

Using the valuation methods of tangible book value, price earnings ratios, and comparison to competitors, Onity is significantly undervalued.

While Onity is in a competitive industry, it is operating well and hedging its risks.

Management is competent and is trying to increase shareholder value. It appears that Onity is going to be moving into a period of share buy-backs now that it is solidly profitable, has simplified its balance sheet, and has reduced debt.

The two main risks are decreases in interest rates, and poor operations.

[1] This is not exactly right. Onity’s total equity is $482m. Total assets are $16,531m. Of this are $2,636m of intangible assets that are the book value of the MSR that Onity has purchased on the open market, and that are adjusted quarterly on a mark-to-market basis. This value adjusts as market conditions adjust, much like the value of a bond adjusts. There is a direct link between the value of these MSR’s and the expected future payments from the MSR’s. While these assets are contracts, they are contracts linked directly to expected future cash flows – again, much like bonds. I include these assets at tangible book value even though they don’t meet the strict definition for tangible assets.