consorcio ara

Price per share at posting: P$4.30 Date of posting: Feb 25, 2025

NOTE: All values below are in pesos.

The Business

Consorcio ARA (ARA.MX) is a Mexican homebuilder that acquires and develops land reserves, constructs housing communities, and sells finished units across entry-level, mid-market, and high-end segments.

In 2025, ARA completed 6,214 homes. As of December 31, 2025, it owned 29.7 million square meters of land reserves, sufficient to build approximately 112,747 homes. These projects are diversified across Mexico.

In addition to residential development, ARA owns and operates six shopping centers[1].

In 2025, ARA generated revenues of P$8,254m. Of this, 95.2% came from residential operations and 4.8% from shopping center operations and land sales.

The Simple Value Story

As of December 31, 2025 ARA’s tangible book value was P$15,702m and its current market value is P$5,436m.

If ARA were to trade at tangible book value, the stock would increase 188%.

Moreover, tangible book value likely understates current economic value.

ARA’s 29.7 million m² land reserve is carried at P$4,595m. These parcels were accumulated over more than 20 years and are recorded at historical price paid. Using a FIFO framework — matching land acquisition timing with development volumes and adjusting by the Mexican housing price index — I estimate the land is understated by approximately P$2,500m.

That implies:

Adjusted land value: P$7,095m

Adjusted tangible book value: P$18,202m

Adjusted tangible book per share: P$14.88

If the market re-rates the company to this adjusted tangible book value, the implied upside is 235%.

For two decades, ARA has been run conservatively. That discipline allowed the company to remain solvent through an extremely volatile period for Mexican homebuilders. The tradeoff has been a stagnant equity valuation and a persistent discount to book value.

In 2023, leadership transitioned from founder Germán Ahumada Russek to his son, Alducín. The new CEO has indicated an intention to accelerate construction activity and better monetize land reserves. Early evidence suggests movement in that direction. Revenues grew 16% in 2025, and management has guided for further growth in 2026.

In 2025, ARA earned P$906m in net income. At a market value of P$5,436m, the stock trades at roughly 6x earnings. A re-rating to 10x earnings would imply approximately 66% upside. Quarterly earnings also accelerated through 2025, reaching P$354m in Q4.

To summarize:

ARA is profitable.

Earnings are growing.

The stock trades at ~6x earnings.

The company trades far below tangible book value.

Tangible book value likely understates the economic value of the land.

The valuation gap is large. The business is stable. The balance sheet is conservative. As revenue and net income continue to grow the valuation gap could close.

Historical Performance

ARA was founded in 1977, in Mexico City, by Luis Felipe Ahumada Russek. He was the president and CEO until 2023, when his son replaced him as CEO. Russek ran ARA conservatively. He steadily built ARA’s land holdings and book value, kept debt low, and survived many Mexican financial crises over the last 49 years.

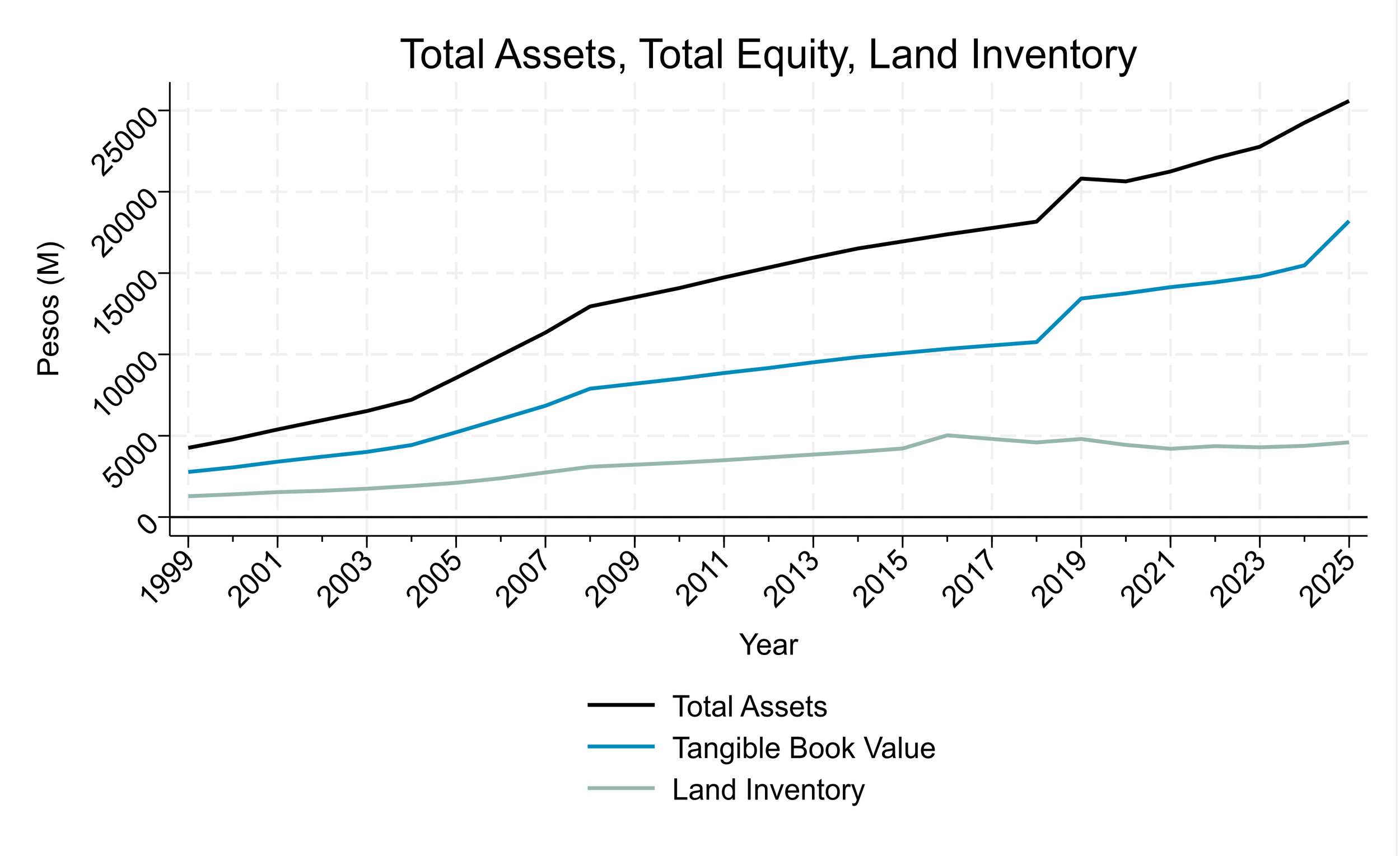

The following figure presents ARA’s total assets, total tangible equity, and its land inventory. Note the steady increase in all three.

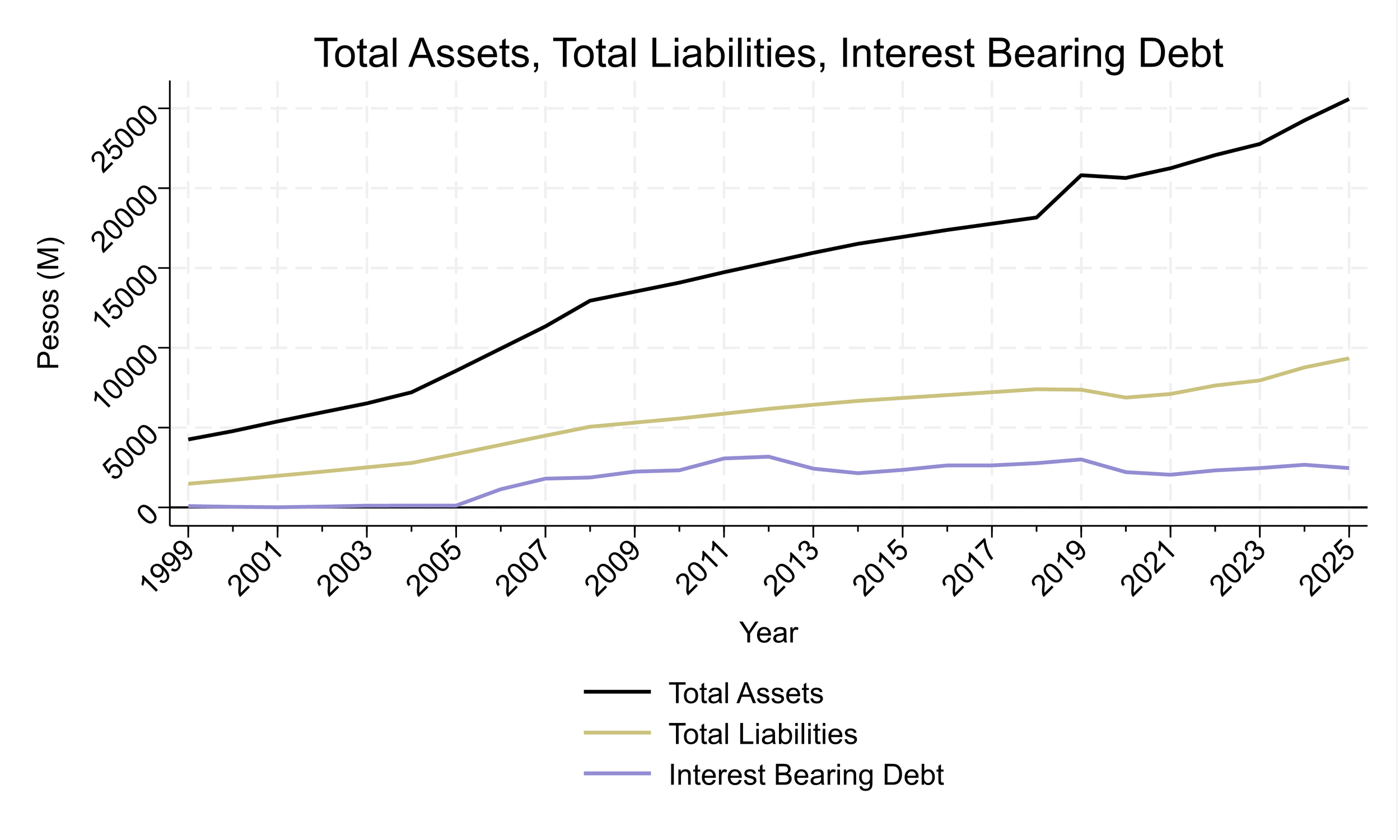

The following figure represents ARA’s total assets, its total liabilities and interest-bearing debt. Note that total assets are well in excess of total liabilities, and the interest-bearing debt is quite low and steady.

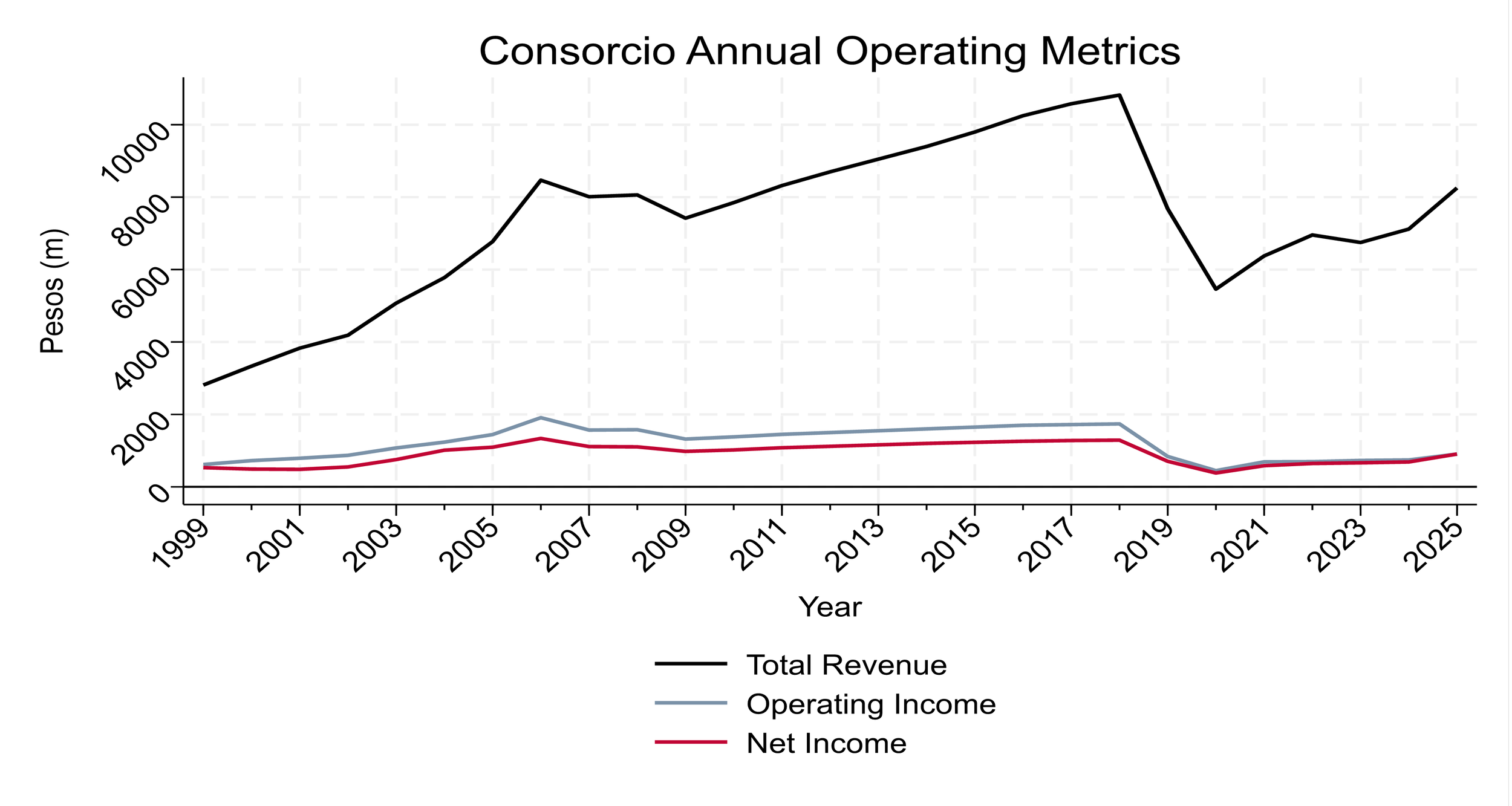

The following figure presents ARA’s annual revenue, operating income and net income for the last 26 years. The dramatic drop in revenues and income in 2019 and 2020 was the result of a country-wide recession in housing in 2019, and then Covid in 2020. It is illustrative of ARA’s conservatism that even in these extreme periods it remained profitable..

The following chart presents ARA’s stock price for the last 25 years. Despite some large intermediate movements in the stock price, the long run outcome is that there has been very little overall appreciation in the stock price in 26 years.

Estimation of Market Value of Land

ARA’s land inventory is recorded at historical acquisition cost. As of December 31, 2025, land reserves are carried on the balance sheet at P$4,595m. The company has accumulated these reserves steadily over more than two decades.

Because land is recorded at purchase price and not marked-to-market, the carrying value likely understates current economic value. Over the past 20+ years, both consumer prices and residential real estate prices in Mexico have increased meaningfully. The question is not whether prices have risen, but by how much the historical cost basis diverges from present value.

To estimate current land value, I constructed a simple framework:

Use annual housing production data and reported lot inventory to estimate the vintage of land holdings.

Assume FIFO land usage — i.e., older parcels are developed first.

Apply the Mexican housing price index to adjust each estimated vintage forward to current prices.

Because land prices have generally increased over time, using a FIFO land usage assumption understates the holding period of certain parcels and therefore produces a conservative estimate of current market value.

Using this approach, I estimate that ARA’s current land inventory has a market value of approximately P$7,095m, rather than the reported book value of P$4,595m — a difference of roughly P$2,500m.

If this estimate is directionally correct, tangible book value is understated by the same amount. Adjusted tangible book value would therefore be approximately P$18,202m. This estimate simply adjusts historical cost to reflect observed housing price inflation. As such, it may still be conservative.

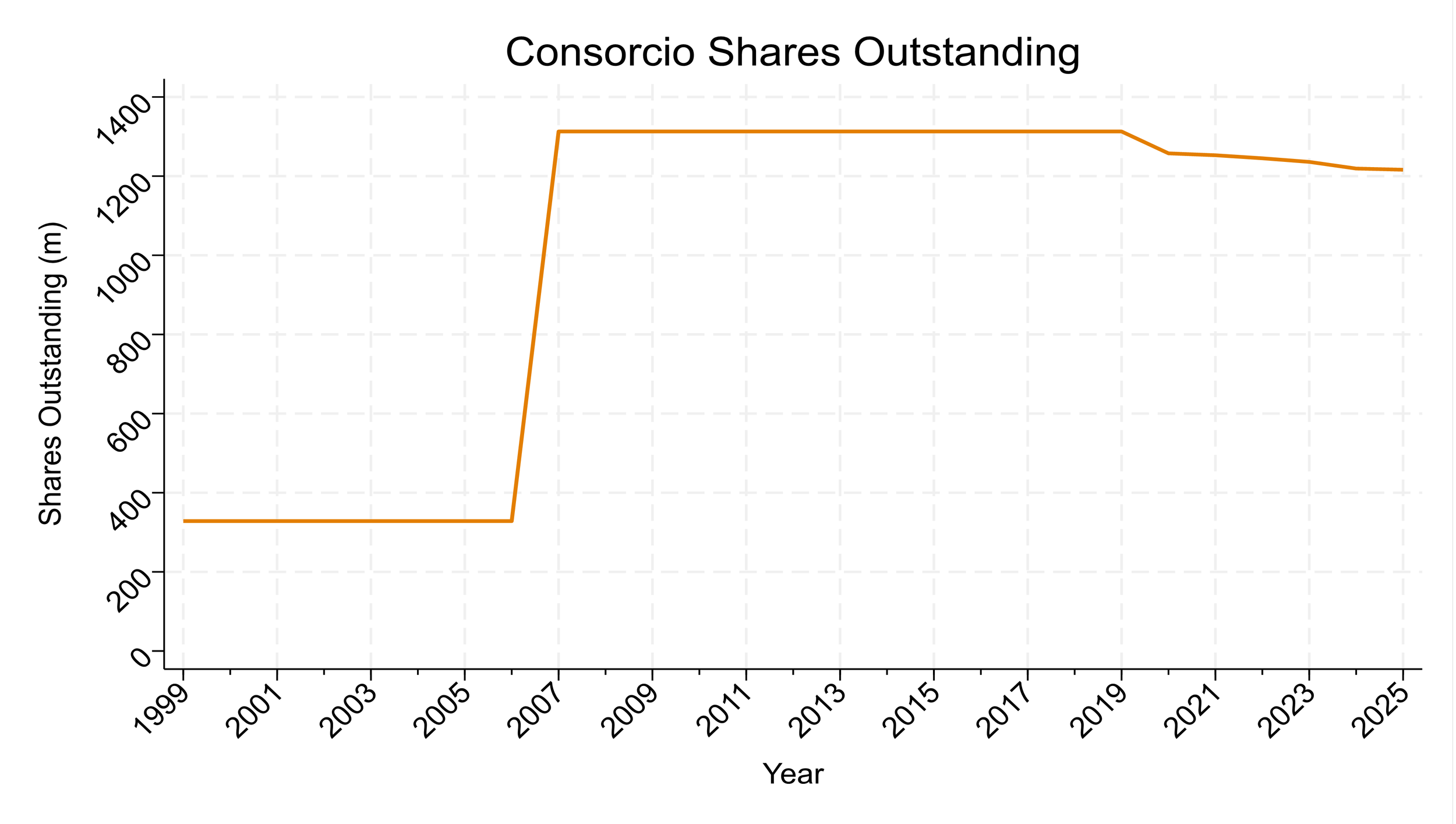

Shares Outstanding

The following chart presents ARA’s shares outstanding for the last 26 years.

Six years ago, ARA began modest share repurchases. Over these six years ARA has repurchased 97m shares (7.4% of outstanding shares). The CEO indicates that share repurchases will continue, but there is no guidance about the amounts or timing.

Dividends

In 2025 ARA restarted dividend payments. In total it paid P$200m, P$0.16 per share (a 3.7% return at current stock prices). ARA indicates it will continue to pay dividends in 2026.

Evidence of Revenue and Earnings Growth

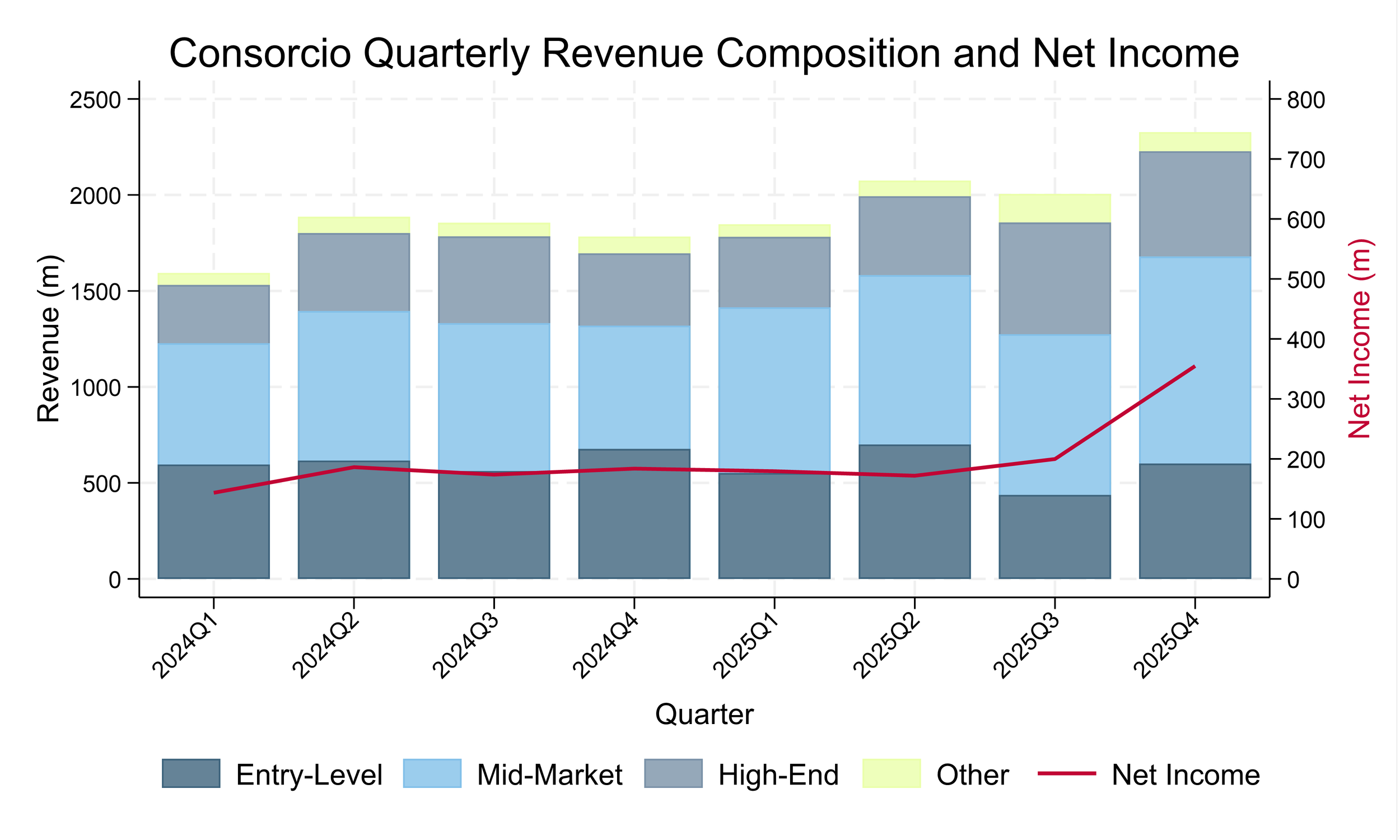

The current CEO, Alducín, assumed leadership in 2023 and has indicated an intention to increase construction activity, shift product mix upward, monetize land holdings, and increase capital returns. The following figure presents quarterly revenue by segment, stacked, with quarterly net income shown on the right axis.

Several patterns are visible.

First, total revenue is increasing. Full-year revenue rose from P$7,119m in 2024 to P$8,255m in 2025 (16% growth). Additionally, quarterly revenue accelerated through the year. Q4 2025 revenue was approximately 30% higher than Q4 2024.

Second, the composition of revenue appears to be shifting. Mid-market (“Medio”) revenue represents a growing share of the total. This shift toward higher-priced homes should support highr margins if sustained.

Third, “Other” revenue has increased. This category includes shopping center operations and land sales. While shopping center revenue has grown modestly, most of the variability appears to come from land sales. This is consistent with management’s stated goal of better monetizing land reserves.

Most importantly, net income has accelerated alongside revenue. As shown in the figure, quarterly net income increased steadily throughout 2025, reaching P$354m in Q4. Full-year net income rose from P$687m in 2024 to P$906m in 2025, a 32% increase.

Whether Q4 represents a new run-rate or a temporary spike remains to be seen. However, the direction of change in both revenue and earnings is clear. If this trend persists, even modestly, the stock price should increase.

Mexican Housing Backdrop

SHF (Sociedad Hipotecaria Federal – Mexico’s government-owned housing development bank) cites a housing backlog on the order of 8.38 million homes. The current federal administration has launched the Programa de Vivienda para el Bienestar, explicitly targeting a step-up in housing construction and related support mechanisms.

On the private-market side, BBVA’s real-estate outlooks describe a market where underlying demand exists, but outcomes depend heavily on mortgage availability and affordability. BBVA notes the housing market softened in 2023, improved in 2024, and was mixed in 2025—with mortgage growth earlier in the year (helped by Infonavit – Mexico’s government-backed hosing finance institution) but renewed pressure later as prices rose and mortgage activity cooled.

Valuation

ARA trades at a substantial discount across multiple valuation frameworks.

First, the company’s market value of P$5,436m is approximately 35% of reported tangible book value (P$15,702m). A re-rating to tangible book would imply approximately 188% upside.

Second, if land holdings are adjusted to estimated market value using the FIFO-based framework described above, tangible book value increases to approximately P$18,202m. Under that estimate, the market value represents less than 30% of adjusted tangible book value.

Third, ARA earned P$906m in 2025. At the current market capitalization, the stock trades at roughly 6x earnings. Even a modest expansion to 10x earnings — still conservative relative to many listed homebuilders — would imply approximately 66% upside.

ARA is looks cheaper than its largest peers. Vinte Viviendas, a publicly traded Mexican homebuilder with a similar operating focus, trades at a book-to-market ratio of approximately 0.6 and at roughly 24x earnings. ARA’s book-to-market ratio is approximately 2.9, and its P/E is 6. Vinte has increased shares outstanding and carries higher leverage, while ARA has reduced shares and maintains relatively low debt.

ARA trades at a deep discount to its accounting assets, an even deeper discount to estimated economic assets, and at a low multiple of current earnings despite improving profitability.

Risks

The main risk is that something negative happens to the Mexican economy or real estate market. This is definite possibility. Mexico is mired in tariff uncertainty from President Trump’s threats. Recently Mexican cartels have caused widespread disruptions. Mexico has had a series of shocks over the last 30 years.

The second risk is that ARA will revert to its past conservative operating methods.

Conclusion

Consorcio ARA represents a profitable, asset-rich, conservatively financed homebuilder trading at a substantial discount to both accounting and estimated economic value.

The balance sheet is strong: Tangible book value is nearly three times current market value. Even without adjusting land values, the company trades at a deep discount to stated equity.

At the same time, ARA is earning positive and growing net income. The stock trades at roughly 6x earnings despite revenue growth, improving mix, and accelerating quarterly profitability. Modest multiple expansion alone would yield meaningful upside.

The downside case appears limited by low leverage, significant land reserves, and a long history of disciplined capital management.

The investment thesis ultimately rests on whether the current leadership continues to increase construction activity, monetize land holdings, and return capital to shareholders. If operating momentum persists and capital allocation becomes more assertive, the valuation gap is likely to narrow. If not, the stock may continue to trade at a discount despite asset backing.

At the current price, the asymmetry is favorable.

[1] Actually, wholly owns and operates 4 shopping centers and owns a 50% interest in two other shopping centers.